The Reality Check: Why Your Broker Choice Matters More Than Your Strategy

Let me show you something that happens more often than most traders care to admit.

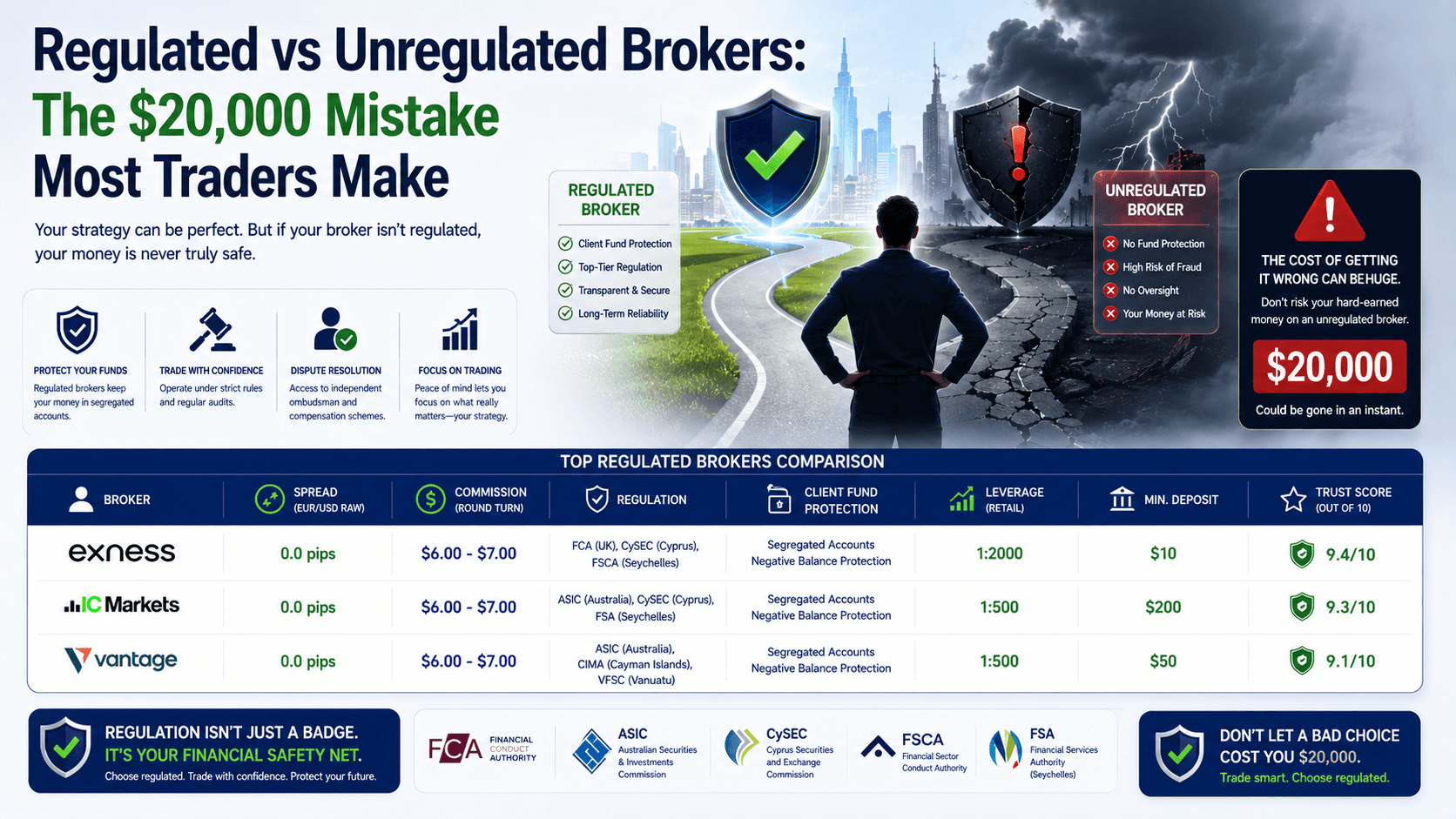

A trader deposits $5,000 with an unregulated broker. The platform looks professional. Spreads are tight. Leverage is generous — 1:500. Everything feels right.

Then one day, they try to withdraw $2,000 in profit. The withdrawal request sits in "pending" for two weeks. Then a month. Customer support stops responding. Eventually, the broker's website goes offline entirely.

That $5,000 — and the $2,000 in unrealized profit — is gone. No recourse. No compensation. No one to call.

This isn't a hypothetical. It's a pattern that plays out repeatedly in the forex industry. And it's the single most important reason why understanding the distinction between regulated vs unregulated brokers isn't just academic — it's the difference between protecting your capital and losing it.

What Actually Defines a Regulated Broker?

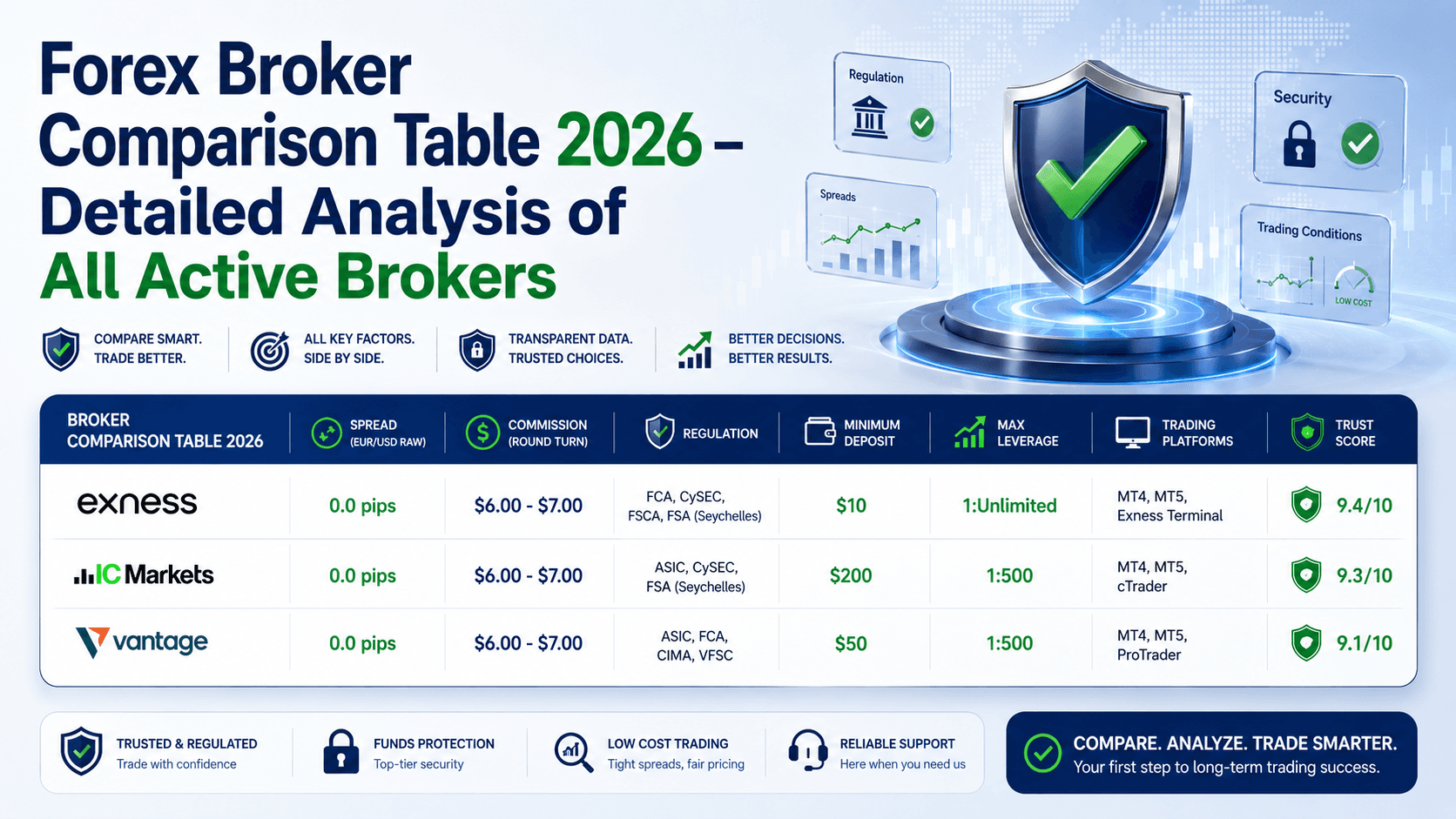

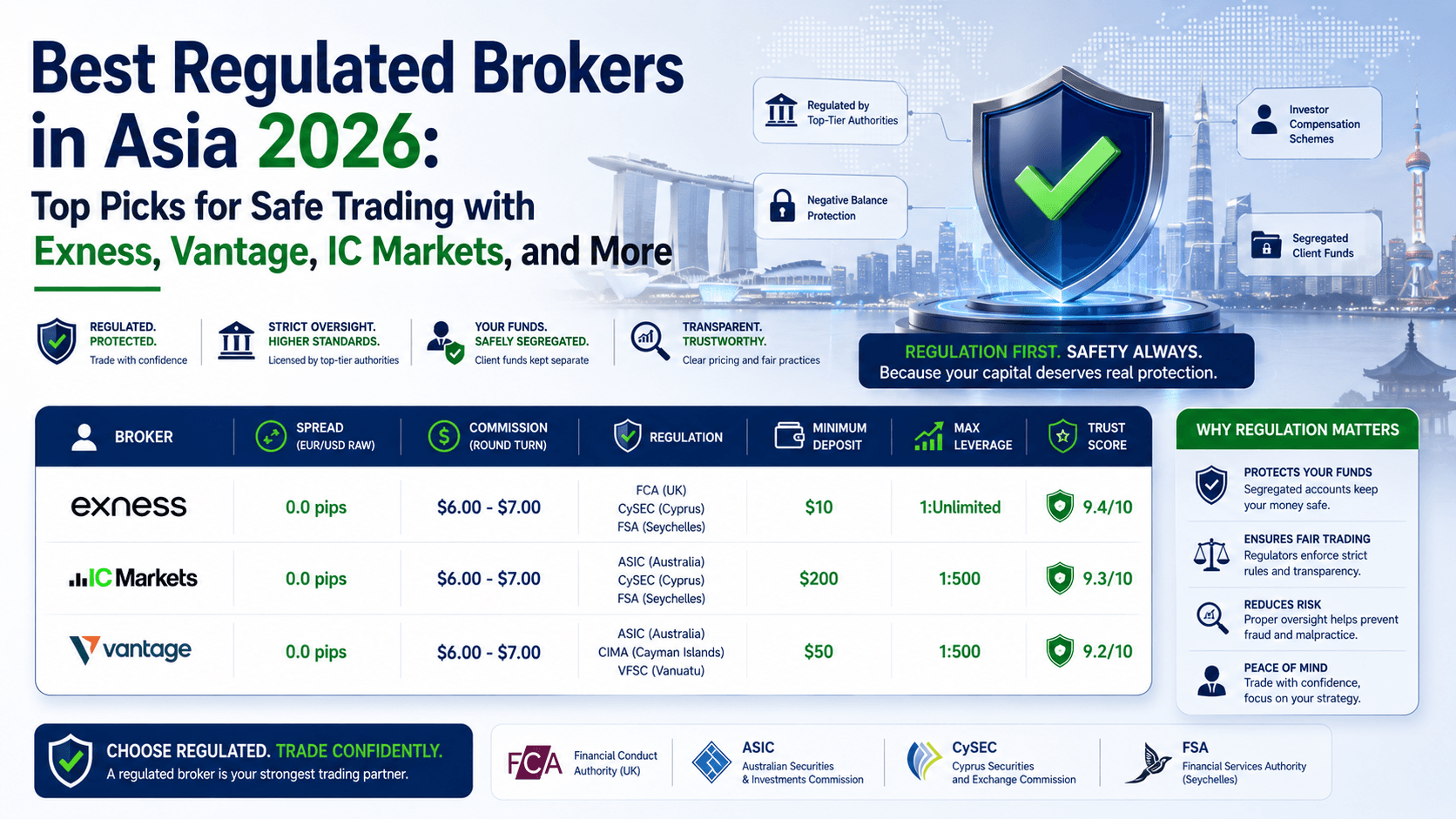

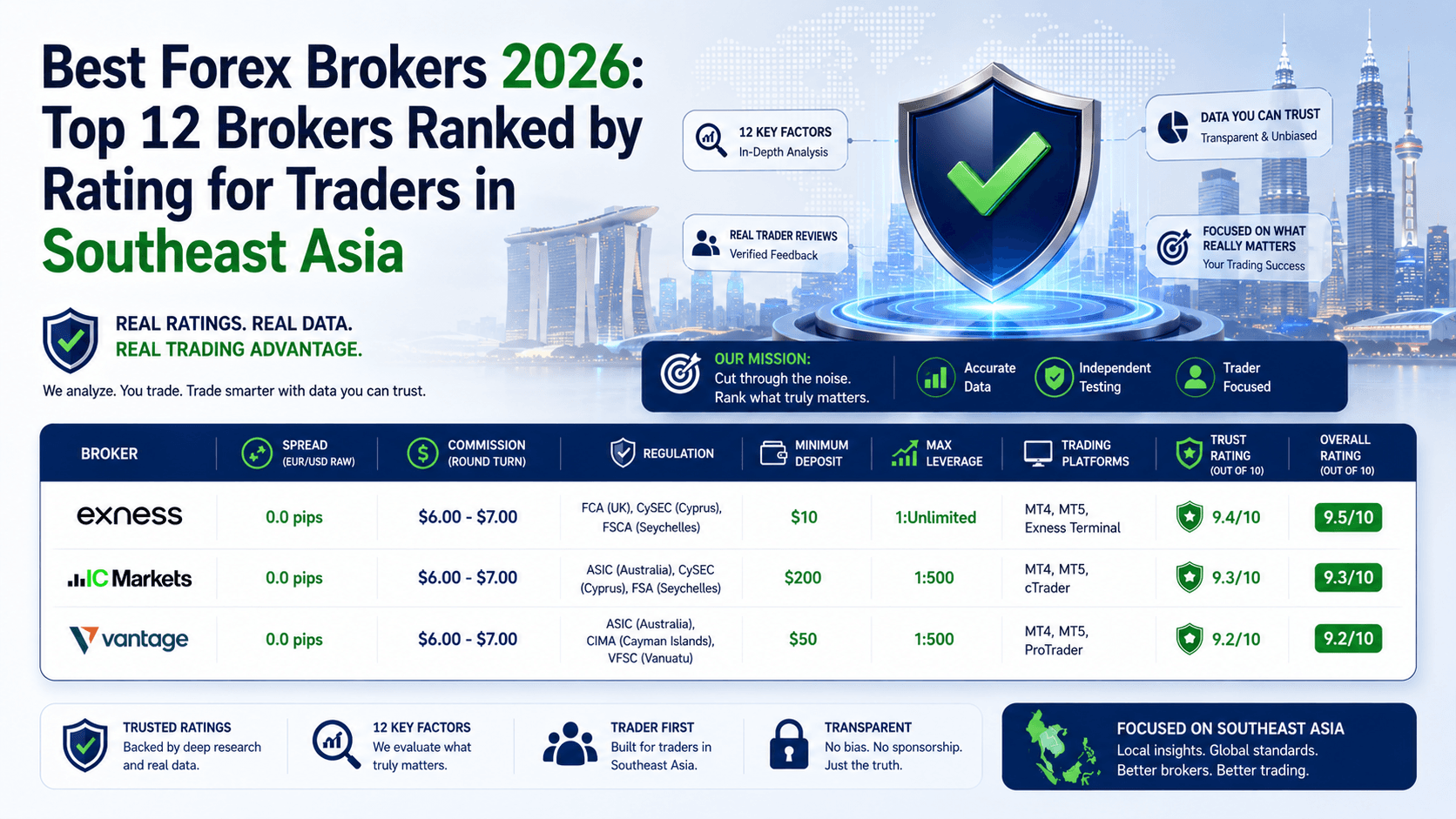

A regulated broker is a financial institution licensed and supervised by an official regulatory body. These bodies — like the Financial Conduct Authority (FCA) in the UK, the Australian Securities and Investments Commission (ASIC), or the Cyprus Securities and Exchange Commission (CySEC) — impose strict operational standards that brokers must follow.

The requirements are not optional. They include:

- Client fund segregation — Your money must be held in separate accounts, away from the broker's operating funds

- Capital adequacy requirements — Brokers must maintain minimum levels of capital to ensure solvency

- Regular reporting and audits — Financial statements are submitted to regulators periodically

- Compliance with anti-money laundering (AML) and know-your-customer (KYC) protocols

- Access to independent dispute resolution mechanisms

These aren't suggestions. They're legal obligations. Violations can result in fines, license revocation, or criminal prosecution.

What About Unregulated Brokers? (And Why Traders Still Use Them)

An unregulated broker operates without oversight from any recognized financial authority. They typically register in jurisdictions where forex trading is not regulated — commonly referred to as offshore jurisdictions.

Why would any trader choose an unregulated broker? The answer usually comes down to two factors:

- Higher leverage — Unregulated brokers can offer leverage of 1:500, 1:1000, or even higher, while regulated brokers in major jurisdictions cap leverage at 1:30 or 1:50 for retail clients

- Fewer restrictions — No limits on trading styles (like scalping or hedging), lower minimum deposits, and faster account opening

But here's the trade-off: that higher leverage comes with a fundamentally different risk profile. When you trade with an unregulated broker, you're essentially trusting them with your money based on nothing more than their word.

The Numbers Don't Lie: A Side-by-Side Comparison

| Factor | Regulated Broker | Unregulated Broker |

|---|---|---|

| Client fund protection | Segregated accounts, often with compensation schemes (e.g., FSCS up to £85,000) | No guarantee — funds may be commingled with broker's operating capital |

| Leverage limits | Capped (e.g., 1:30 for major pairs under ESMA, 1:50 under ASIC) | Unlimited in practice (1:500, 1:1000 common) |

| Transparency | Mandatory disclosure of spreads, execution policies, and financial health | Variable — often minimal or misleading information |

| Dispute resolution | Access to independent ombudsman or regulator | No external recourse — you're on your own |

| Accountability | Subject to audits, fines, and license revocation | No oversight — broker can disappear overnight |

| Withdrawal reliability | High — regulated brokers must process withdrawals promptly | Low — delays, fees, or outright refusal are common |

The Wrong Way vs. The Right Way

The Wrong Way: The "Better Deal" Trap

A beginner trader sees an unregulated broker offering 1:500 leverage on a $500 account. They think: "With this leverage, I can control $250,000 in position size. I'll make money fast."

They deposit $500. They open a position on EUR/USD with 0.5 lots — way too large for their account size. A 20-pip move against them wipes out $100, or 20% of their account. Within a week, the account is gone.

But even if they had a winning trade, the broker might refuse to pay out. The leverage was the bait. The trap was the lack of protection.

The Right Way: The "Slow and Safe" Approach

An experienced trader opens an account with an ASIC-regulated broker. They start with $2,000. Maximum leverage is 1:30. They trade 0.05 lots on EUR/USD — a position size that gives them a 20-pip stop loss worth only $10 in risk.

They don't get rich overnight. But they also don't lose everything. Over six months, they grow the account to $2,400 — a 20% return. More importantly, they can withdraw that profit whenever they want. The money is safe.

The difference isn't intelligence. It's understanding that regulated vs unregulated brokers isn't about which offers better terms — it's about which protects your capital.

How to Verify a Broker's Regulatory Status

Verification is straightforward if you know where to look:

- Check the broker's website footer — Legitimate brokers display their license number and regulatory body prominently

- Visit the regulator's official website — Search for the broker's name or license number in the regulator's register of authorized firms

- Cross-reference with third-party sources — Platforms like the FCA's Financial Services Register or ASIC's Professional Registers are reliable

- Look for warning signs — If a broker claims regulation but provides no license number, or the license number doesn't match the regulator's records, that's a red flag

Major regulatory bodies and their registers:

- FCA (UK) — Financial Services Register

- ASIC (Australia) — Professional Registers

- CySEC (Cyprus) — CySEC Regulated Entities

- CFTC/NFA (US) — BASIC (Background Affiliation Status Information Center)

FAQ

Is it illegal to trade with an unregulated broker?

No, but it depends on your jurisdiction. In many countries, trading with an unregulated broker is not illegal for the trader — but the broker itself may be operating illegally. The risk is entirely on you.

Can unregulated brokers ever be trustworthy?

Some operate honestly, but there's no external mechanism to verify this. Without regulatory oversight, you have no guarantee of fair treatment, fund safety, or dispute resolution. The risk far outweighs any potential benefit.

Do regulated brokers charge more in fees?

Not necessarily. Many regulated brokers offer competitive spreads and no hidden commissions. The cost difference is often negligible compared to the security you gain.

How can I check if a broker is really regulated?

Always verify directly on the regulator's official website using the license number provided by the broker. Never rely solely on the broker's own claims.

Quick Recap

- Regulated brokers are licensed by official authorities and must follow strict rules on fund segregation, transparency, and dispute resolution

- Unregulated brokers operate without oversight, offering higher leverage but with no guarantee of fund safety or fair treatment

- Verification is essential — always check a broker's license number on the regulator's official register

- The cost of a mistake is high — losing your entire deposit to a broker that disappears is a risk no trader should take

Quick Win: Verify Your Broker in 5 Minutes

Open your broker's website. Scroll to the footer. Find their license number and the regulatory body that issued it. Go to that regulator's official website and search for the license number. If it matches, you're safe. If it doesn't, start looking for a regulated alternative today.